America Can’t Build AI Without China’s Permission

Half of 2026 data centers are delayed. The bottleneck isn’t chips — it’s transformers.

The AI buildout doesn’t have a chip problem. It doesn’t have a capital problem. It has a transformer problem.

Half the data centers planned for 2026 won’t open on time. Not because the money ran out. Because a piece of equipment that costs less than 10% of the project — and takes five years to deliver — hasn’t arrived.

The country racing to dominate artificial intelligence can’t manufacture the electrical hardware to plug it in.

The Numbers

— 30–50% of US data centers planned for 2026 will be delayed or canceled (Sightline Climate, April 2026).

— Of 12 GW expected online this year, only 5 GW is under construction. 16 GW remains “announced” with no visible progress.

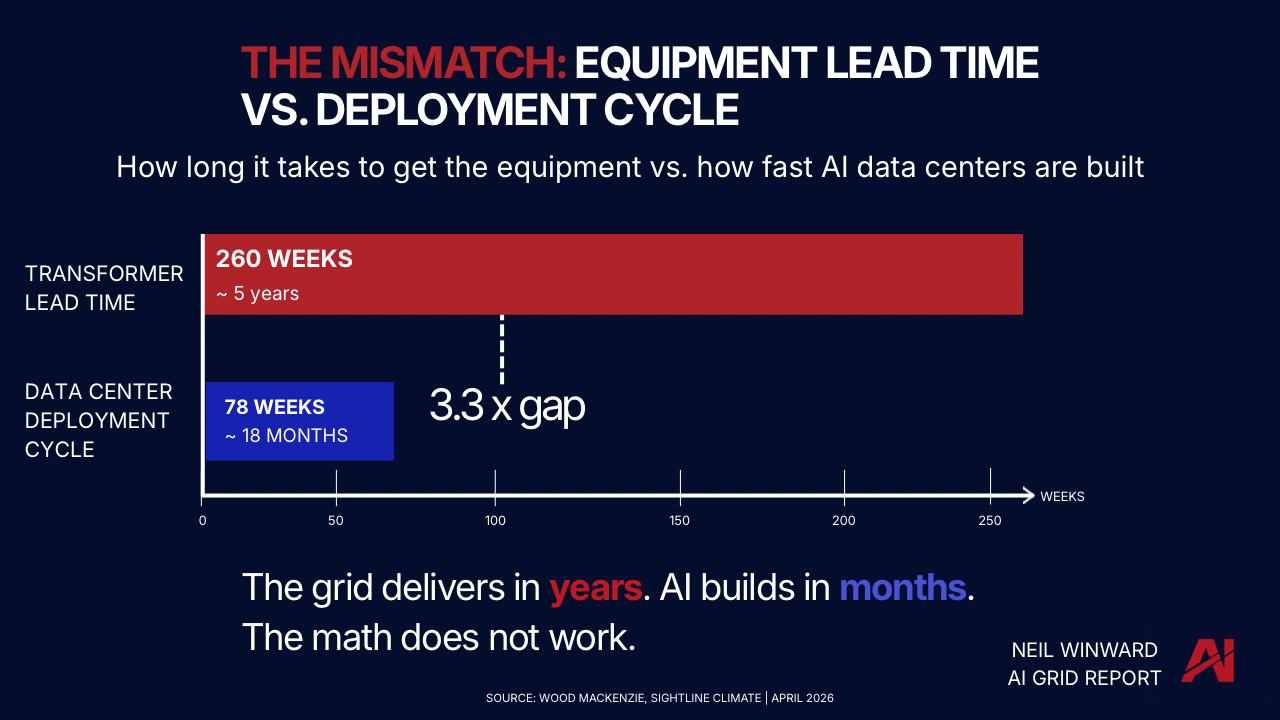

— Power transformer lead times: 128 weeks average. Generator step-up transformers: 144 weeks. Data center deployment cycle: under 78 weeks.

— Chinese transformer imports to the US surged from 1,500 units in 2022 to over 8,000 through October 2025 — a five-fold increase in three years.

The standard narrative says the AI constraint is chips, or capital, or models. That framing misses where the physical system binds.

The constraint is electrical equipment. Transformers step voltage down for data center use. Switchgear distributes power safely. Batteries smooth demand spikes that degrade chip equipment. Without these components, a data center is a building with no purpose — like a highway with no on-ramps.

And the US can’t make enough of them.

The Delay Wall

Here’s the math that should concern anyone underwriting AI infrastructure timelines.

Sightline Climate (a tactical intelligence platform for energy transition decision-makers) tracks 140 large data center projects targeting 16 GW of capacity by year-end 2026. Only 5 GW is under construction. The rest sits in a pre-construction limbo where announcements run years ahead of physical capability.

This isn’t new. In 2025, manufacturers delayed 26% of announced capacity and pushed back commercial operations for another 10%. The pattern is consistent and accelerating (per Techspot): for 2027, more than 25 GW has been announced, but fewer than 10 GW is under construction. For 2028–2032 (per Futurism), 37 GW of planned capacity has no firm completion date. Only 4.5 GW has broken ground.

Capital is available. Land is available. The electrical equipment to connect these facilities to the grid is not.

The gap between announced capacity and construction is widening, not closing.

The Equipment Bottleneck

Think of transformers like rebar in a building. Nobody talks about rebar. It’s maybe 3% of total construction cost. But if the rebar doesn’t show up, you don’t have a building — you have a pile of expensive concrete.

Transformers are the rebar of the AI buildout.

Lead times for high-power transformers have stretched from 24–30 months pre-2020 to as long as five years. AI data center deployment cycles run under 18 months. That’s a 3.3x gap between what the buildout needs and what the supply chain delivers.

Electrical infrastructure represents less than 10% of total data center cost — but a single delayed component halts the entire project.

The China Dependency

The US imports approximately 80% of its power transformer supply and 50% of its distribution transformer supply. In January 2026, US utility executives visited a Chinese transformer factory and found roughly half the units on the floor flagged for American delivery — some destined specifically for data center companies.

Chinese transformer exports to the US increased by 182% in the first two months of 2026 alone. China’s share of US battery imports remains above 40%. Its share of certain transformer and switchgear categories sits at approximately 30%. Power transformer demand is up 116% since 2019. Generator step-up transformer demand is up 274%.

A decade of reshoring initiatives has not moved the needle. The US faces a 30% supply deficit in power transformers and a 10% deficit in distribution transformers.

Despite every policy signal pointing toward decoupling, the physical dependency is deepening.

Here’s what most infrastructure analysis misses: the equipment bottleneck isn’t just a supply problem. It’s a demand convergence problem.

Six sectors are competing for the same transformers and switchgear simultaneously. US electricity demand is up 7% since 2020, reversing a decade-long decline. Solar deployments are up 400%+ since 2019. More than half of US distribution transformers are past their expected service life. Billion-dollar weather events rose from 8 in 2014 to 27 in 2024.

The AI buildout isn’t competing against a shortage. It’s competing against five other structural demand drivers for the same hardware — and the full scale of that collision is worse than most models assume.

Anyone modeling data center timelines without a transformer procurement sensitivity is not modeling the proper constraint. They’re modeling the press release.

Tariffs have made this worse, not better. Steel tariffs have raised transformer prices approximately 20%. Copper tariffs of 50% inflate costs for both imported and domestically manufactured units. The US has one domestic producer of grain-oriented electrical steel (steel in which the grain lines up with the direction of travel of the magnetic field) — AK Steel (Cleveland-Cliffs). The highest-grade material still has to be imported.

OEMs have announced $1.8 billion in capacity expansions since 2023. Siemens Energy committed $1 billion to US manufacturing. GE Vernova committed $600 million plus a $5.3 billion Prolec GE acquisition. These are real investments. But the demand growth rate means they’re running to stand still.

“It’s going to be a long battle. It’s not something that can be solved in the next five years.” — Ben Boucher, Wood Mackenzie

AI Grid Constraint Index — Preview

The equipment bottleneck doesn’t hit every region equally. Some ISOs have pre-ordered transformer inventory 36 months out. Others are still waiting on deliveries that were due in 2024.

That divergence is already showing up in our regional scoring. Regions with secured equipment pipelines and shorter interconnection queues are pulling ahead. Regions dependent on Chinese imports with no domestic backup are falling behind — and tariffs are accelerating the split.

This week’s Constraint Index update tracks:

• which regions have locked in transformer and switchgear delivery — and which are exposed to the 5-year lead time wall

• where the equipment bottleneck is already binding on energization timelines

• the two regions where our score moved this week — one tightening, one stabilizing

The full Constraint Index with regional scores, capital sensitivity notes, and the methodology breakdown is available to subscribers.

Most analysis stops at “demand is growing.”

That’s not where the problem is.

The problem is that six industries need the same hardware, one country makes most of it, and the policy response is raising the price of the hardware we can’t make ourselves.

This week’s full analysis covers:

• The full demand convergence breakdown — 455 GW of competing demand for a supply chain sized for a fraction of that

• Why the Gulf AI bet — $2.2 trillion in pledges — just hit a wall that has nothing to do with technology

• The Stargate Abilene case study: what happens when GPU cycles outpace grid timelines

• Which electrical infrastructure equities are positioned for the convergence, and why pricing power is structural

• The helium wildcard most semiconductor analysts aren’t tracking

→ Full analysis available to subscribers

Which data center project in your pipeline has the most unrealistic equipment procurement timeline? Serious question — we’re tracking this.