MISO Has a Retirement Problem

MISO is scheduled to retire ~25 GW of generation. Michigan alone loses ~3 GW of coal before 2029 and ~6 GW by 2032". DTE Energy (DTE) projects up to 8.4 GW of new data-center load on the same wires.

Where We Are in the Walk

Six issues in, the AI Grid Report (TAGR) has covered the methodology, the macro tariff and Gulf threads, and the first two regional deep dives.

→ Issue 04 — ERCOT. The Lone Star grid clears its interconnection queue at near-zero withdrawal. Connect-and-manage interconnection, no centralized capacity market, one regulator. Texas doesn’t have PJM’s auction problem; it doesn’t have auctions.

→ Issue 06 — PJM. The capacity auction cleared at the ceiling. Twice. PJM’s queue doesn’t clear; ERCOT’s does. Same demand. Same generation. Different process.

This week, we’re looking at MISO (Midcontinent System Operator)— the largest physical footprint on the US grid by territory, stretching from Manitoba to northern Louisiana.

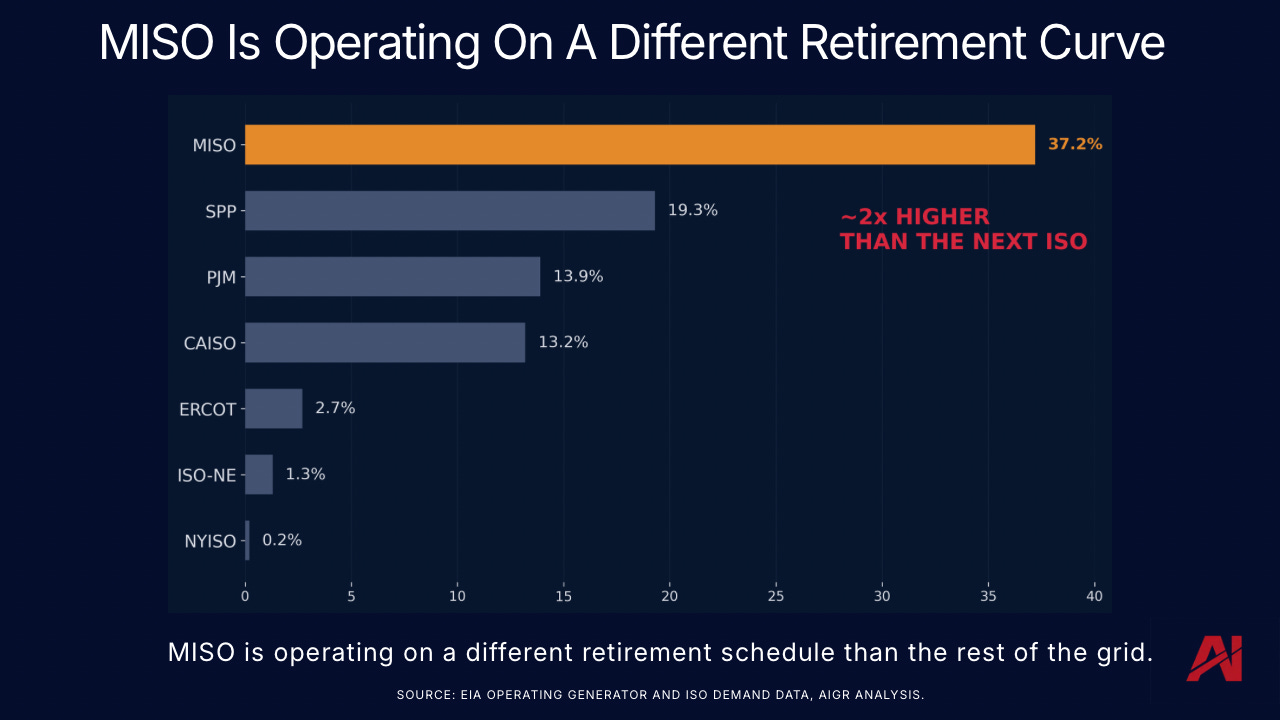

MISO’s headline number is not an auction price.

It is a retirement schedule.

The Number

~25 GW of MISO operating generation is on a planned retirement schedule. That is roughly 37% of MISO’s average demand.

No other major ISO is close.

SPP is next at roughly half the exposure. PJM sits in the mid-teens. ERCOT — despite being the fastest-growing load center in the country — remains below 3%.

MISO has its own retirement problem.

What’s Leaving

The 25 GW is concentrated.

Subbituminous coal accounts for roughly 14 GW. Natural gas adds another ~8 GW.

Nuclear is notably absent from the near-term retirement schedule. Xcel’s Monticello plant — the one obvious candidate, previously scheduled to retire in 2030 — received NRC (Nuclear Regulatory Commission) approval in February 2026 to operate through 2050. Prairie Island is in line for similar treatment. MISO’s nuclear fleet has been materially de-risked at the same time the dispatchable coal and gas fleet is leaving.

The issue is not simply the volume of retirements.

It is the type of generation leaving the system.

Much of what’s retiring is dispatchable, fuel-secure capacity that can operate through extended weather events, peak demand periods, and low renewable output conditions (i.e., no sun, no wind).

That distinction becomes critical once replacement timing starts slipping.

What We Are Diving Into This Week

ERCOT cleared its queue. PJM cleared at the ceiling. MISO has not had to clear either.

What MISO has is firm capacity leaving the system on a posted schedule, while much of the replacement remains trapped in the queue rather than connected to the grid.

In this week’s premium article, we’ll show which plants are retiring, which utilities own them, what the replacement queue actually contains, and why replacing coal megawatts with renewable megawatts is not a one-for-one exchange.

We’ll also cover the news thread that may have quietly turned MISO’s retirement schedule from a posted plan into an active planning problem — and why the fourth federal emergency order on a single Michigan coal unit may be the precedent the rest of the 2028 fleet now has to underwrite against.

Keep Reading ->