The Market That Can’t Clear

PJM cleared at the cap for a second time. The system is pricing a shortage it can’t fix.

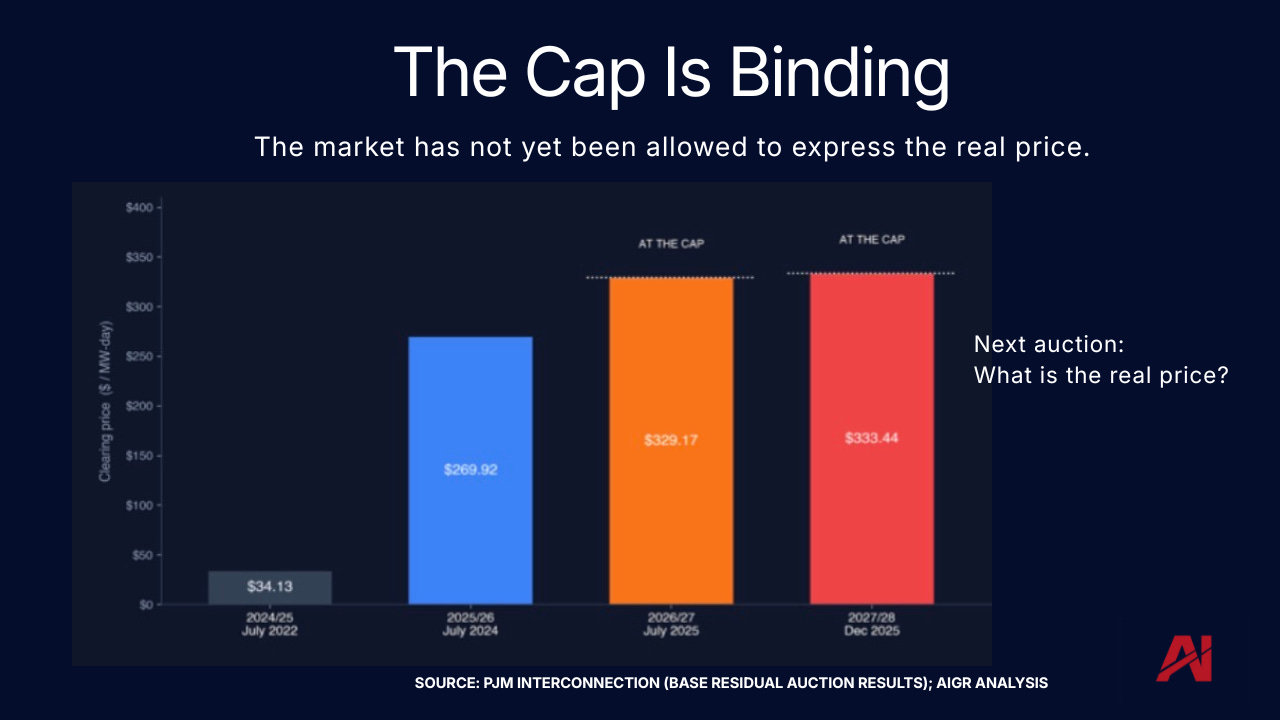

PJM cleared at the cap. Again.

The system keeps finding the ceiling. It hasn’t found the solution.

On December 17, 2025, PJM’s capacity auction cleared at $333.44 per megawatt-day.

That is the cap.

It is also the second consecutive PJM auction to clear at the cap. The previous auction, held in July 2025, cleared at $329.17. Both auctions hit the price ceiling that FERC set in late 2024 to keep residential bills from a sudden jump.

Together, those two auctions secured 134,479 MW of capacity for $16.4 billion of annual payments — at a procured reserve margin of 14.8%, the lowest in PJM’s history.

That number is now the most-watched price in US electricity.

It is also a price the system has never actually been allowed to discover.

It is also, increasingly, the price that determines whether AI infrastructure is built on schedule.

The Cap Was Extended — Again

The cap was supposed to be a temporary instrument. It is now in its fourth consecutive year.

On April 28, FERC approved PJM’s request to extend the price collar for two more delivery years — 2028/29 and 2029/30. The extension keeps the cap at roughly $325/MW-day and the floor at $175/MW-day, the same parameters that capped the last two auctions. Without it, PJM had estimated the next auction’s price cap would have defaulted to about $550/MW-day.

When PJM holds its next Base Residual Auction this summer, the cap will still be in place. The auction after that — in December — will be capped too.

PJM’s Base Residual Auction (BRA) procures capacity three years ahead of delivery. The December 2025 auction cleared capacity for the June 2027–May 2028 delivery year. The summer auction clears for June 2028–May 2029. The December auction clears for June 2029–May 2030. All three are now capped.

The forward gap exists so generators can build new supply for a known revenue stream. Except the forward gap is now shorter than the build cycle for new gas generation, which is the structural problem the rest of this issue describes — and which is why FERC extended the cap. New supply cannot arrive in time, so the cap stays on to protect ratepayers from the price the auction would otherwise produce.

The market still does not know what an uncapped clear looks like. It is now four years since it last did. The two capped auctions were already records.

What would the market actually clear at without the cap?

$400? $500? Higher?

There is no consensus — only suppressed price discovery.

The auction is clearing at the ceiling. The price hasn’t been allowed to move.

Same Demand. Same Generation. Different Process.

On the supply side, firm capacity is exiting faster than it is being replaced (or, at least, trying to exit). On the demand side, ~5,250 MW of new load arrives every year inside PJM’s forecast — almost all of it is data centers.

The clearing price is the cost of that gap — the dollar value, expressed per MW per day, of every megawatt of firm capacity PJM needs but doesn’t have. When supply is short, the price rises until enough supply (or enough demand response) is willing to commit. When the gap is structural — firm supply exiting faster than replacement — the price keeps rising until something stops it. This time, FERC stopped it with a cap.

In ERCOT, the same supply technologies, the same data center developers, and the same hyperscale tenants run through a queue that clears fast.

In PJM, two-thirds of projects in the queue never reach completion.

The queue is full. Most of it never meets its intended load.

That is the entire difference between a $333 / MW-day capacity clear and a market—ERCOT— that doesn’t pay for capacity at all.

If PJM and ERCOT are running the same technologies, why does one system convert and the other stall?

Is it structure, governance, or execution?

In This Week’s Edition

This week breaks down:

• what is leaving PJM (~5,500 MW of fossil capacity scheduled to retire — Brandon Shores, H.A. Wagner, Conemaugh, Keystone) — and why scheduled retirements are not real retirements

• what is replacing it (2.1 GW in 2025, almost entirely solar)

• how Northern Virginia became the place where the December auction price was decided

• what FirstEnergy’s Energize365 program — a $36B transmission build-out by PJM’s largest transmission owner — tells us about the supercycle hiding inside the auction print

• what ERCOT does differently — and which parts of it PJM can copy

The full Constraint Index shows which PJM zones are most exposed to the next auction, and which signals to watch going into the summer auction.

Continue reading: