Transferable Tax Credits Are Quietly Reshaping Infrastructure Capital

The tax credit may be the mechanism, but the larger story is how capital influences which physical systems are built.

Most wealthy investors think about taxes as something minimized quietly in the background.

That framing understates what’s happening. The transferable tax credit market reached $42 billion in 2025, up 27% from $32 billion in 2024. When tax equity and preferred equity are included, total tax credit monetization hit $63 billion. The market grew through OBBBA (Trump Administration signature tax legislation passed in 2025) reconciliation, not despite it.

But there is a more strategic question in this conversation:

If you are going to write the check anyway, what exactly do you want your capital funding?

A ballroom? Or a power plant?

That question sounds rhetorical until you look at how transferable tax credits are working inside the real economy.

What’s changing is not the desire to reduce taxes. That has always existed.

What’s changing is the realization that the tax code is the policy tool that influences which physical systems are built.

The §6418 transferability provision in the 2022 IRA opened a market that didn’t exist before. The transferability mechanism survived the 2025 OBBBA reconciliation. Eligibility rules tightened — meaning the pool of qualifying projects narrowed — but the buyer-side market remained intact. Some credits were eliminated; some had their eligibility windows shortened; some of the eligibility criteria, especially around foreign content, were tightened. The window that exists today is real, but it is not the same window that existed in 2024.

A transferable tax credit is usually described as a financial instrument. Technically, that is true. Economically, however, it is beginning to function more like a directional signal for capital allocation into energy, manufacturing, grid infrastructure, and industrial capacity.

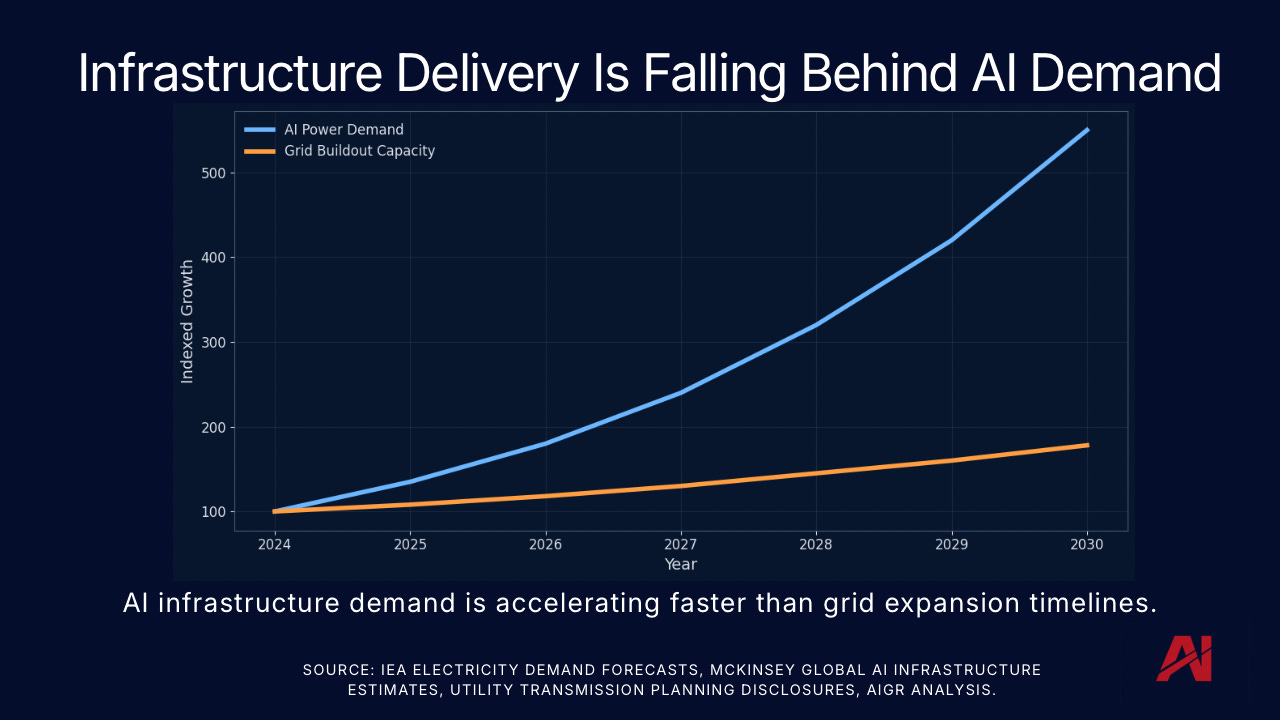

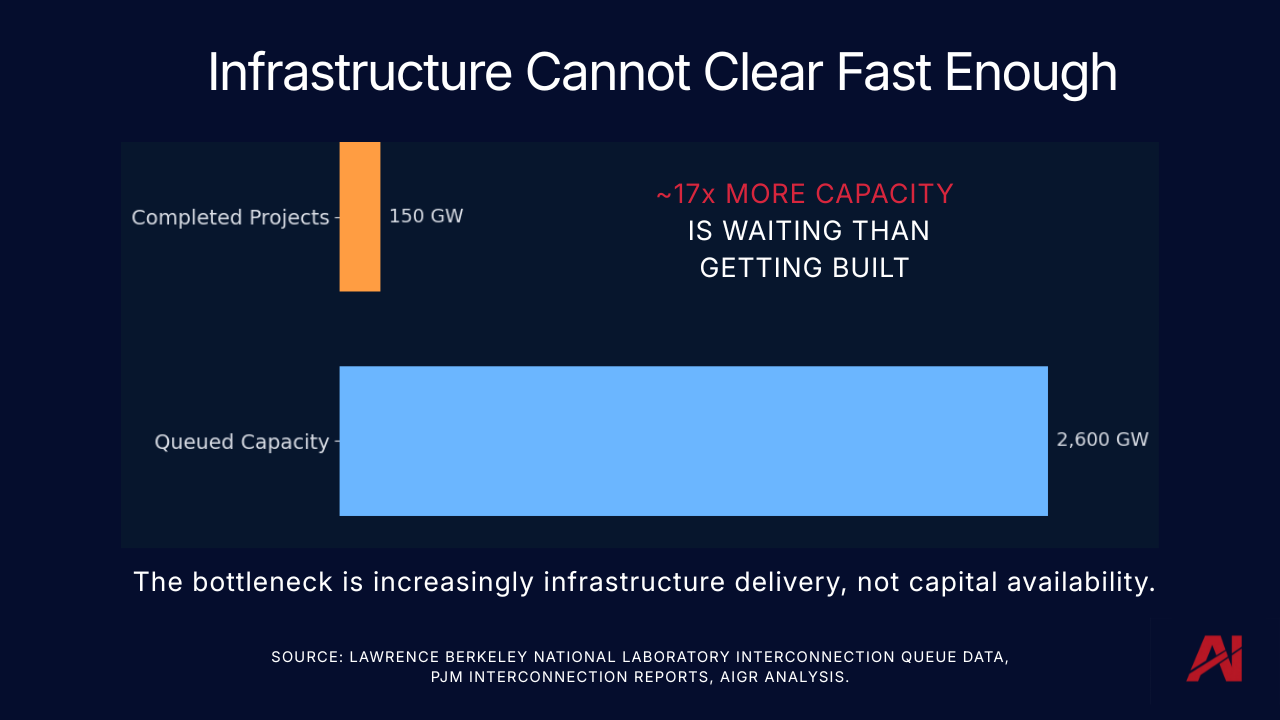

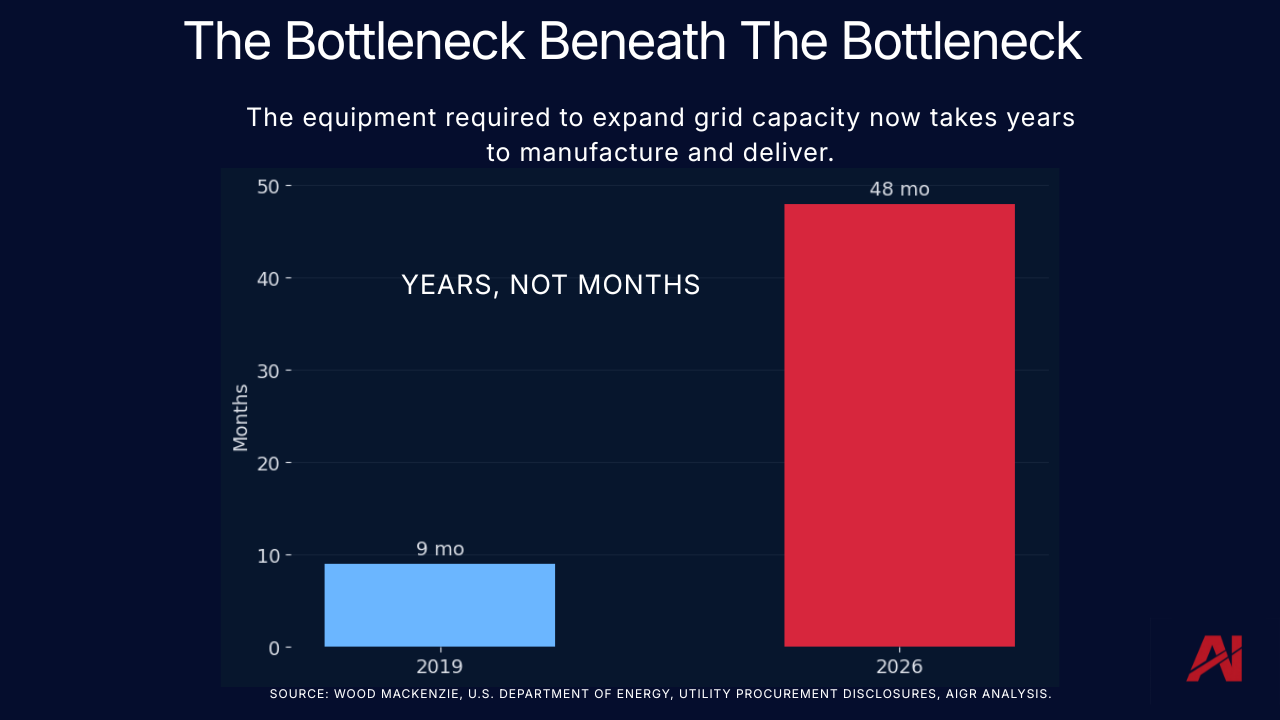

The U.S. is entering a period where physical infrastructure constraints are dominating economic outcomes in a way the financial markets are just beginning to price.

The constraints appear in transformer shortages, interconnection delays, transmission bottlenecks, power availability, natural gas infrastructure, and generation lead times that can’t be resolved on software timelines.

Data center expansion timelines are accelerating faster than transmission and grid delivery capacity. That reality is changing how capital evaluates long-duration opportunity.

Capital Is Becoming More Intentional

Family offices, private investors, and long-duration pools of capital are no longer thinking purely in terms of quarterly returns.

Many are asking a different question:

“What systems do we want our capital to support?”

The U.S has entered a period where enormous amounts of physical infrastructure need to be rebuilt, expanded, or modernized simultaneously.

The AI buildout alone is exposing how underbuilt the grid really is.

Data centers require massive injections of power. Power at that scale depends on transmission, transformers, substations, permitting, land access, and infrastructure investment cycles measured in years rather than quarters.

The Grid Is Quietly Repricing Everything

This is particularly visible inside energy infrastructure. Unlike the software cycles that dominated the last decade, the outcomes here are physical and measurable — whether a transmission corridor is built, a generation project reaches commercial operation, or grid capacity expands has direct consequences for industrial growth, electricity pricing, and regional competitiveness.

Stocks like Eaton, Vertiv, and Schneider have traditionally been seen as downstream of the AI buildout. Not anymore — they are the gating layer, and the market has noticed. All three have broken out of long-term ranges to the upside, which confirms the thesis but does not, on its own, signal current entry points. The structural story and the entry timing are separate questions.

The market spent the last decade believing software was the bottleneck.

The bottleneck is becoming physical infrastructure. The result is that electricity itself is beginning to reprice.

It means the real opportunity is not simply “AI.”

It’s the underlying physical systems required to support it.

Transferable tax credits are directing capital toward those systems.

If electricity becomes constrained by transmission and deliverability rather than generation alone, how should infrastructure itself be valued relative to the applications sitting on top of it?

Family Offices May Be Uniquely Positioned

Large institutions and public markets often struggle with long-duration infrastructure cycles because the timelines rarely align cleanly with quarterly expectations. Family offices, however, can operate with substantially longer investment horizons.

The structure fits family offices unusually well. The infrastructure cycle is long-duration, illiquid, politically shaped, and operationally complex — conditions many quarterly-managed pools of capital struggle to underwrite.

That dynamic makes the current environment particularly interesting because the underlying infrastructure cycle will not resolve quickly.

Grid expansion doesn’t occur on software timelines.

Transmission projects can require seven to ten years to complete, transformer manufacturing capacity can’t expand overnight, and AI-driven power demand is rising inexorably.

That mismatch creates long-duration investment opportunities tied to hard assets, constrained systems, and real economic necessity.

The Psychology Is Changing Too

Historically, taxes were viewed primarily as something minimized quietly in the background through accounting strategies, portfolio structuring, and conventional tax planning.

Some investors are now beginning to ask a different question:

“Is there a more focused, intentional way to allocate tax dollars while still complying with tax policy?”

Transferable tax credits stop feeling like accounting exercises and begin functioning more like participation in a national industrial buildout tied to energy infrastructure, manufacturing capacity, grid resilience, and domestic economic expansion.

Investment structures carry clearer accountability than the metrics that have dominated philanthropic and ESG-scoring frameworks. A transferable tax credit settles against a placed-in-service date, a real project, and a real tax liability. An ESG score reflects a methodology the rating agency can revise after the fact.

The opportunity is no longer viewed exclusively through the lens of tax reduction or financial optimization, but through participation in the construction of systems that are strategically important to the economy itself.

That change in mindset may ultimately become one of the defining characteristics of this cycle.

Why This Matters Beyond Taxes

The market still tends to describe transferable tax credits as niche financial instruments.

What is emerging is a system in which tax policy, infrastructure constraints, industrial strategy, energy demand, and capital allocation are becoming intertwined.

The immediate question is whether this cycle produces attractive returns. The credits themselves are purchased at a discount — that’s the market incentive— and that discount is tax-free—that’s the policy tool. So, in practical terms: a $5 million tax liability becomes $4.5–4.6 million in credits directly funding a real infrastructure project with a placed-in-service date. The project exists before the capital arrives. The accountability is built in from the start.

That discount alone may not move the needle for family office allocators—though it has created a powerful enough incentive to have established a $42 billion market in two years, mostly for corporations— but pair it with the idea that taxes can be redirected toward causes and infrastructure projects family offices genuinely want to support, and the equation starts to look very different. The larger question is whether it changes how sophisticated investors think about participation in the construction of physical systems. “My taxes fund national parks” is no longer an aspirational joke at a cocktail party. “My taxes fund the energy buildout (and not a ballroom)” is a legitimate claim.

If infrastructure becomes the limiting factor behind AI, manufacturing, and industrial growth, what happens to the value of the systems that make all three possible?

The AI Grid Report

AI Grid Report is an independent research publication focused on the intersection of energy infrastructure, AI-driven electricity demand, grid constraints, industrial policy, and long-duration capital allocation. Recent editions have covered ERCOT, PJM, MISO, interconnection bottlenecks, transmission constraints, and the physical infrastructure dynamics increasingly shaping economic outcomes across the US energy system.

If these themes interest you, you can subscribe to AI Grid Report here →

About Dakota Ridge Capital

Dakota Ridge Capital works with family offices, private investors, and strategic capital navigating the energy and infrastructure buildout — including direct access to transferable tax credit opportunities tied to real projects already in development.

If you are evaluating how your capital allocation intersects with the infrastructure cycle, the conversation is worth having before the next reconciliation window closes.

Request a private briefing → https://www.dakotaridgecapital.com/contact-us

Really fascinating piece. Transferable tax credits feel like one of those “behind-the-scenes” financial innovations that most people overlook, but they could fundamentally change how climate and infrastructure projects get funded. The most interesting part is how they’re opening the market beyond just large banks and institutional players. Quiet policy shifts often create the biggest long-term economic ripple effects.