What America Is Trying to Build

The future US power system is already visible in the interconnection queue.

What the queue is, and why it matters

An interconnection queue is the waiting list for new power plants trying to connect to the grid.

But it is more than a backlog.

Every project in the queue has already committed capital, entered a multi-year approval process, and accepted the possibility of transmission-upgrade costs before it can deliver power. In practice, the queue is a map of what developers believe is worth building — and where they believe future electricity demand will justify the wait.

That matters because the queue increasingly reveals a very different picture of America’s future grid than most public policy debates do.

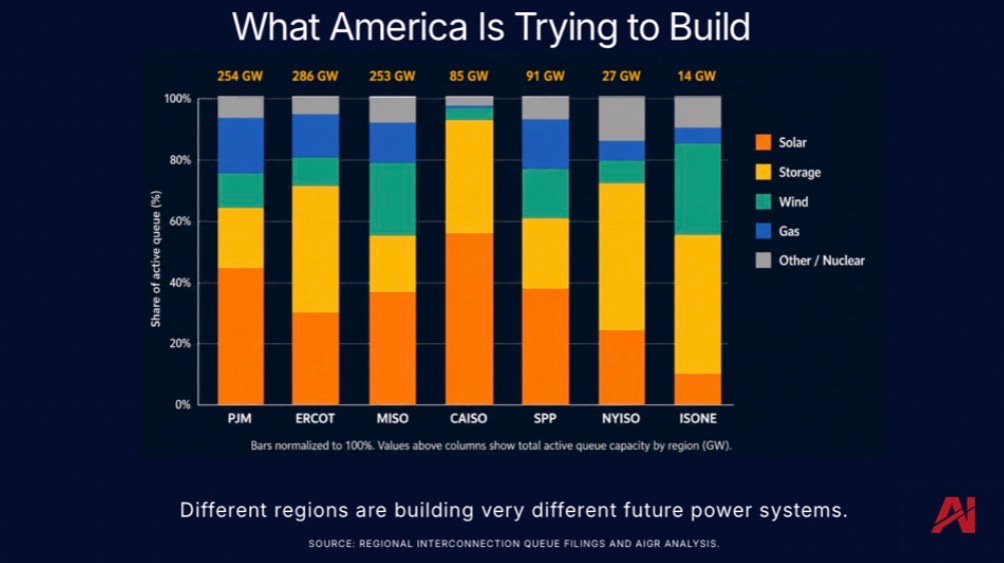

Across the country, developers are attempting to build massive amounts of:

solar

battery storage

gas generation

transmission-connected AI infrastructure

while coal has almost completely disappeared from new development plans.

The U.S. power system is fragmented across regional grid operators. Seven major regions — including PJM, ERCOT, MISO, CAISO, SPP, NYISO, and ISO New England — publish detailed project-level queue data. Together, along with the non-ISO Southeast and Western utility regions, they represent nearly all US electricity generation.

The scale is enormous.

Roughly 1,400 GW of generation and 890 GW of storage — 2,290 GW combined — sit in active US interconnection queues as of end-2024, per Lawrence Berkeley National Laboratory (LBNL — a US Department of Energy national lab whose Electricity Markets and Policy group publishes the annual Queued Up interconnection report). Solar represents the largest share of proposed capacity, followed by battery storage. Gas remains meaningful but regionally concentrated. Wind is increasingly uneven by geography. Coal is almost absent.

The queue does not guarantee these projects will ultimately be built.

But it does reveal something extremely important: what the market believes the future grid will need.

What the composition implies

Coal is not underrepresented in the queue; it’s almost absent.

The existing coal fleet still operates. Some plants continue clearing in PJM’s capacity auctions, while others remain online under reliability agreements that delay retirement. They’re reliable; they’re necessary, but they’re politically toxic. Developers are no longer attempting meaningful new coal capacity in any major U.S. interconnection queue.

What replaces it is where the regions diverge.

ERCOT is building solar and storage in roughly equal proportions. PJM shows a broader mix of gas, solar, storage, and a small but unusual cluster of nuclear projects. MISO’s newer queue cycles tilt more heavily toward gas than its earlier renewable-heavy cycles. CAISO, NYISO, and ISO New England show almost no new gas development at all.

The same country.

The same physics.

The same Inflation Reduction Act.

Different bets.

Why the queue matters

The queue is not a forecast of what will ultimately be built.

Withdrawal rates remain high across most regions, and projects reaching commercial operation often spend years moving through the interconnection process. The queue reflects what developers are attempting — not what will necessarily survive.

But that still makes it one of the most important forward indicators in the power market.

Every project in the queue has already passed an economic screen. Capital has already been committed. Developers have already decided the opportunity is worth years of waiting, study costs, and potential transmission-upgrade exposure.

That is a very different signal from:

a press release

a policy target

a utility planning document

a political speech

The queue is capital already moving toward the grid.

What this issue covers

This week’s premium section will explain:

why some regions are still building dispatchable supply while others are not,

why storage exploded across the queues, and

what the interconnection data may already be revealing about the future shape of the US grid.

Continue Reading